+30 Insights from VCs for the New Cycle

- Name

- The Datafi

- Published on

- · 15 min read

Name: The Datafi

Published on April 2023

Summary: This article analyzes the correlation between cash flow - VC investment appetite and market development through each cycle/round of funding and each category. This article also identifies the VC investment trends within 7 ongoing narratives, comprehends the new season - new order - new strategy in VC investments, and presents some insightful perspectives about VC that you may not be aware of.

INTRODUCTION

>> Data Context

This report employs two types of data: Off-chain and On-chain.

- On-chain Data:

- On-chain data reflects investment behaviors and trends on DEX (excluding wallets of Market Maker funds like Jump Trading, Wintermute, Alameda Research, or funds with OTC selling activities like Amber and FalconX).

- Total VCs considered: 121 out of 125 VCs, considering 967 wallets out of 2,025 wallets.

- Off-chain Data:

- Off-chain data reflects VC investment trends and market rules. Note that it includes individual investor data aligned with VC funding rounds, collectively referred to as VC.

- In total, over 5,143 VCs and more than $87 billion were invested in 3,817 projects from 03/2019 to 03/2023. These figures were compiled from Messari + Defillama, and reprocessed by our team (correcting and supplementing the data).

>> Personal Perspectives of VC

Based on insights gathered from insiders and practical observations, DataFi wishes to share the following viewpoints:

- Not all projects need to raise funds from VCs; numerous founders invest from their own pockets. Therefore, VC data certainly does not reflect all projects in the market.

- VCs primarily hold Governance tokens for a greater say in project expansion/mergers with other entities. Project teams tend to hold more Utility tokens to proactively add value to their tokens..

Nevertheless, for larger funds, the priority isn't necessarily holding governance tokens, but rather the "value it brings" > "the amount invested to hold it".

- VCs have two primary roles in a project: MM and Network; Advisor and Fund. In reality, few VCs can be effective advisors when the project team understands the internals the best. Not every VC has a large enough capital to enter the seed/private rounds of major projects, so the fund might not always play a major role. The core lies within the VC's network: the ability to connect with ecosystems, proficient marketing teams being capable of attracting users, and "finding liquidity" for the project.

- To avoid the label of “dump” token, VCs have various legitimate methods to sell the tokens they receive. For instance, lending these tokens to lending pools or selling them on exchanges.

- VCs also endure financial losses when projects fail or when funded projects don't progress through. Consequently, larger funds have built various components within their ecosystem, some of which are openly disclosed, though often ignored until they "pump."

>> Research Team

DataFi's research analyst team comprises Bob, Max, and Rosy.

Our team welcomes feedback and perspectives from readers to progress further. Any input can be sent to:

Admin Rosy (Telegram)

Facebook / Twitter DataFi

Email: thedatafi@gmail.com

Sincerely,

Bob, Max & Rosy (from left to right)

Note: Remember to thoroughly read SECTION C, my dear readers!

A - VC STATS

Below are some highlighted points that DataFi has compiled and calculated, which could contribute to your understanding of Venture Capital during the period from March 2019 to March 2023.

B - VC CASH FLOW & MARKET CORRELATION

I. VC vs BTC & DEFI

Below is a chart illustrating the cash flow of VC capital into various Crypto projects, juxtaposed with the BTC chart and the market cap chart of the Defi sector from March 2019 to March 2023.

Key message/highlight:

- There exists a synchronicity in the growth patterns of VC investment inflow, BTC price, and Defi market cap.

- The BTC price trajectory exhibited an earlier surge compared to the overall market, coupled with early indications of contraction in early 2022 despite continuous VC funding influx (*).

- The Defi market manifests acute sensitivity to VC capital infusion, underscored by several intersecting peaks (May 2021; January 2022; April 2022).

Reflecting upon the four-year span (also coinciding with the BTC cycle, 2019-2022), Defi has emerged as the "narrative" drawing capital into the crypto market. Presently, however, we have not yet answered the intriguing question: what will be the next trend driving new capital into the market?

Another noteworthy aspect from the aforementioned chart is that during the tail end of the BTC price surge, VC capital still substantially flowed into projects. The question emerges: is this a result of VC fomo behavior or merely a belated disclosure of that "capital" to sustain the retail investors' "to the moon" sentiment?

Moreover, the (*) observation above, to some extent, recapitulates the sequence of fund inflow into the Crypto market: initially channeling into BTC → subsequently encompassing Altcoins and low-cap coins. Notably, even when BTC has recently rebounded over 70% from its bottom (16,700 to 29,100), skepticism persists: could sharks be enticing liquidity inflow for a subsequent forceful sell-off?

To foster the investment perspective during this period, readers are advised to peruse the MACRO and MONEY FLOW reports to unveil the profound insights and “revelations” therein.

II. VC vs MARKET SENTIMENT

In an era of burgeoning technological advancements and an expanding Crypto market, shall VC investments follow suit in magnitude and novelty? The ensuing statistics, though not exhaustive, partially elucidate the interrelationship.

1. Investment Budget

BTC price and the average value per fundraising round from March 2019 to March 2023.

AAR/D = Avg. Amount Raised per Deal (average capital raised in a deal, wherein a deal denotes a fundraising round for a particular project)

Key message/highlight:

- During the bullish phase (uptrend + early downtrend), a deal raising less than $25 million is considered low, while during the downtrend, an amount exceeding $14.5 million is perceived as substantial.

- Preceding the new BTC uptrend cycle (2019-2020), although VC capital infusion into the market was not yet robust, there was a spate of deals raising substantial, unprecedented funding (nearly marking the highest value across all deals from 2019 to the present). Can this be seen as a form of "anticipatory bullish season recognition"? (*)

(*) The spikes in December 2019 and February 2020 are attributed to:

- December 2019: Ripple (XRP) raised $200 million, Figure raised $103 million; both projects fall under the Infrastructure and Centralized Finance (Cefi) sectors.

- February 2020: Remarkable funding rounds included Aleo - series B $200 million; Alchemy - series C $200 million; Polygon Studio raised $450 million; Luna Foundation Guard raised $1 billion; Aptos - preseed $200 million, etc. A majority of these projects are situated within the infrastructure sector.

2. Investment Appetite

2.1. Across Funding Rounds

Below Image: The proportion of deals across each funding round. Bottom Image: The proportion of capital raised across each round.

Key message/highlight:

- (1)Throughout 2019 to present, the proportion of deals securing funding in the seed round consistently dominates (~50%) compared to other rounds.

- (2) The count of projects successfully securing funding in the series A, B, C, D rounds remains proportionally small, displaying no pronounced escalation.

- (3) The secured investment rounds such as Series A, B, C, and D overwhelmingly take the bulk of the total VC funding.

The foregoing (1) and (2) analyses potentially indicate an absence of escalating numbers in mature projects. In tandem with (3), this signifies that while VC capital is disseminated across numerous "profit-promising" ventures, substantial investments predominantly gravitate towards projects demonstrating long-term potential and a greater degree of safety.

2.2. Across Categories

Below image: Capital raised per category per month. Bottom Image: Number of deals per category per month. Period: March 2019 to March 2023.

Key Message/highlight:

- VC capital has not yet returned to the market, remaining on a downward trend.

- Although the Defi sector boasts numerous projects, the total capital raised remains the lowest compared to other sectors. In contrast, the Cefi sector presents a converse trend (*).

- During the bearish season, especially post-August 2022, the number of Infrastructure projects experienced a marginal decrease, whereas the Cefi/Defi/NFT sectors witnessed substantial diminutions.

- Infrastructure perpetually remains a prioritized developmental sector, substantiated by the substantial quantum of capital allocated herein, exceeding the investments directed towards NFT/Web3/Defi. Moreover, VC investments in projects within this domain consistently accounted for a stable proportion from February 2021 to March 2023.

- Web3 only received a modicum of VC investment, registers a multitude of projects, even during a downtrend; however, the raised capital is modest (**).

(*) The Cefi sector requires considerable funds and time for establishment, whereas, within the Defi sector, projects can be effortlessly forked, hence they proliferated.

(**) Does Web3 merely represent a speculative facade? This topic will be elucidated further in the Web3 report. Notably, Quarter 1 of 2023 witnessed Web3 as the sector with the highest number of deals (108) and the most substantial capital raised ($814 million) surpassing other sectors. Could Web3 be quietly constructing its foundation amidst the bear market? Are there recognizable indicators? The DataFi team will delve deeper into the Web3 sector later on.

Moreover, the VC capital flow also oscillates in accordance with market sentiment. Hence, when evaluating the funding a project secures, it is essential to consider the sector of the project and the prevailing market sentiment.

Key message/Highlight:

- In the realm of NFTs, during the bullish phase, a funding below $14 million is considered as low, whereas during the bearish phase, exceeding $8 million is considered high (readers should apply a similar analysis to other sectors).

Note: Over time, those figures may change as market size, technology value, etc. change.

- During the previous bullish season, the average funding for a Cefi project was approximately 12 times compared to that of a Defi project.

- During the bearish season, figures in the aforementioned table decreased by around half for both Cefi and NFTs, as well as Web3. However, only the Defi sector bucked this trend, surging by 117%, with AAR per deal surpassing even NFTs and Web3 (*).

(*) An in-depth analysis of the Defi sector reveals three projects that secured significant funding during the bearish phase:

- Lithosphere Network: Raised $400 million in a seed round; its technology enhances smart contracts in the digital economy.

- D-ETF: Raised $50 million, marking the first genuinely decentralized ETF.

- Uniswap: Raised $165 million in series B (October 2022). This milestone for Uniswap coincided with the emergence of the ALM trend - the forthcoming Uniswap V3 fork, accompanied by projects benefiting from this narrative, such as Unipilot, Trader Joe, Algebra Protocol, Stride, SteakHut, Popsicle Finance, ICHI, Gamma Strategies, etc. For those interested, refer to DataFi's on-chain report CDOC.15 for further details.

III. VC vs. TREND & NARRATIVE

Note: The data presented here is focused solely on Ethereum, as it contains the majority of tokens and offers optimized tools for analysis (enhancing data accuracy).

In addition to capital infusion into projects, it's important to examine how Venture Capitalists (VCs) are speculating and trading in the market. Are VCs betting on particular trends or narratives? When did they start? What are the current trends? These questions require on-chain data analysis. In this report, DataFi selected seven narratives that have, are, or may leave an impression on the market for investigation: Gamefi, NFT, AI, LSD, RWA, SocialFi, and Wallet. The findings are as follows:

Number of VCs within each narrative in the first quarter.2023

Key messages / highlights:

As of the present time:

- NFT is the narrative with the highest number of VC participants in the first quarter.

- SocialFi has the lowest VC participation among the seven narratives (n/m total VC of the 7 narratives).

- The number of VCs participating in LSD, AI, and RWA is relatively similar, even though RWA isn't as "hot" as AI and LSD is ongoing.

However, what narratives are VCs currently increasing or decreasing their token holdings in? Providing an exact answer is challenging. Nonetheless, we can consult the following data:

Total VC funding in each narrative per month for the past year (03/2022 - 03/2023)

Key messages / highlights:

- Although NFT and Gamefi are the two narratives with the highest VC participation, they also have the lowest VC funding. These two have decreased slightly over the past year.

- AI, SocialFi, and LSD saw initial VC engagement, followed by a decline, but they experienced a rapid increase from $aM at the start of February 2023 to $bM by the end of March 2023 (a x% increase in just two months).

- AI, SocialFi, and LSD had nearly equivalent VC funding in both February and March 2023. All three experienced significant decreases in early April 2023.

- RWA is a narrative that has seen an increasing balance from early February 2023 until now, which coincides with recent mentions.

Reviewing token prices in these narratives during the first three months of 2023, we can realize:

- AI Group: Prices exhibited strong growth in early February 2023 after a prolonged period of bottoming out. For instance, GRT increased by ~x4, and FET by ~x10. However, both of these tokens subsequently decreased by around 50%. Nonetheless, the balance decreased by ~83%. Does this imply that they exited around 66% of their holdings? Not necessarily, the balance of VC within the AI group (for each token) needs to be considered.

- LSD Group: Experienced similar growth, with LSD and FXS increasing by ~x3. However, the emerging Shanghai story has limited the decrease in token prices (~27%-36%), yet the balance decreased significantly, unlike AI. Could this mean they also sold off their LSD tokens?

Notes:

- The data won't encompass 100% of VC balances due to potential assets being staked, farmed, or locked on other platforms.

- VCs might have invested in these projects earlier but only received vesting (token distribution) recently, meaning they might not be recent buyers.

C - A NEW SEASON, A NEW ORDER, A NEW STRATEGY

In the previous season, we adopted a "backing the right horse" approach, where projects supported by reputable backers were more likely to perform well and soar. Obviously, larger funds have the capability to choose promising projects, and having strong resources and networks assists these projects in executing effective marketing. Relying on tier rankings will still be employed in the new season (if you need this list, you can message us to obtain a reference source).

However, there's an interesting aspect that many might overlook: VCs have two primary roles in a project - MM and Network; Advisor and Fund. In reality, few VCs can serve as effective advisors when the project team themselves possess the deepest understanding of the project's intricacies. Not every VC can access the seed/private rounds of major projects, and therefore, the fund's role might not be as significant. The main influence is within the VC's network - their ability to connect with ecosystems, proficient marketing teams capable of attracting users, and "finding liquidity" for the project. Consequently, when exploring the backers of a project, understanding the fund's role is crucial.

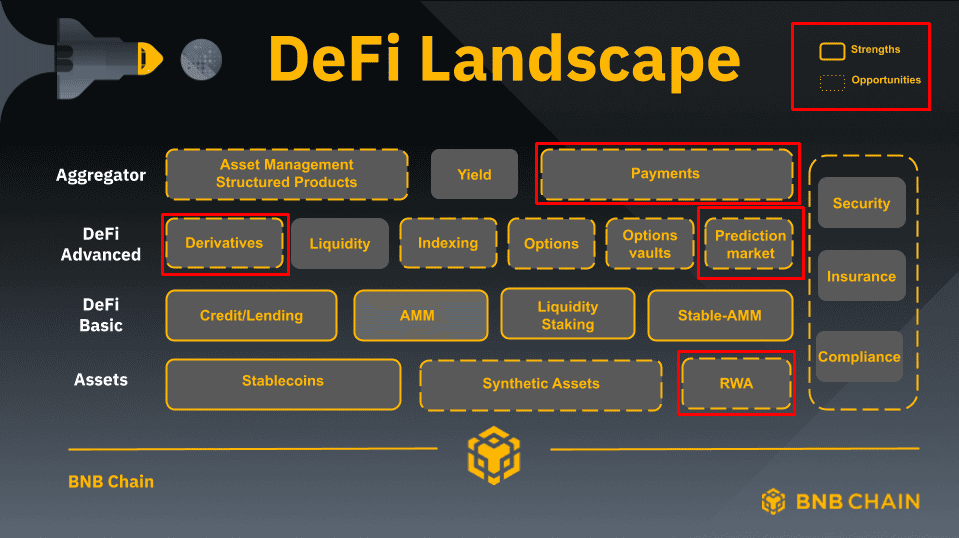

Furthermore, there's a strategy, while not entirely new, that might see more usage in the near future - "following the influential fund that shapes the game." Binance Labs is an example. Did you know that VCs also experience losses when projects fail or when funded projects don't progress? Hence, prominent funds like Binance Labs have created integral components within the BNB chain, not solely depending on identifying new projects. They become the creators of the game, and retail investors like us can follow "cosmic signals" they generate, such as KEY WORDS and TRENDS. The example below illustrates this:

Pieces to focus on for development in 2022 on the BNB chain. Source: Binancians.

From the image, we can recognize the keywords they highlight, such as "MetaFi" (Metaverse & Defi), "Name Service" (in 2023, we witnessed the spotlight on the space ID project ($ID) as BTC increased from $28kxxx to $30kxxx), and many more names filled in the red boxes. A part of this list can be found below:

Digging deeper into the DeFi realm, we can see keywords carrying evident investment opportunities. By the beginning of 2023, the market witnessed narratives about LSD, and the resounding chatter about RWA...

DeFi ecosystem on the BNB chain. Source: bnbchain.org.

Here's an update as of 22/03/2023 regarding opportunities within the BNB Chain, which readers can refer to. DataFi, in particular, focuses on the "BNB Mass Adoption Infra" goal set by BNB for 2023, including Account Abstraction (Social Login, Gasless), Identity Solution, Hybrid Application, Communication layer, and Gaming Infra.

And what about you? What will your strategy for the new season be? Will you follow the flow of funds or narratives, or the macroeconomic rhythm? Don't forget to delve into DataFi's other research regarding these three keywords.

Eventually, the DataFi team wishes you a new journey full of both lessons and achievements! Remember to seek additional insights and opportunities from our team's other research, like Narrative, Big Signal 2 (macro), and Money Flow, which was just published in April 2023.

Thank you, dear readers!

Disclaimer: This article is not intended as financial investment advice.

Additionally, there are some statistics that you might find useful:

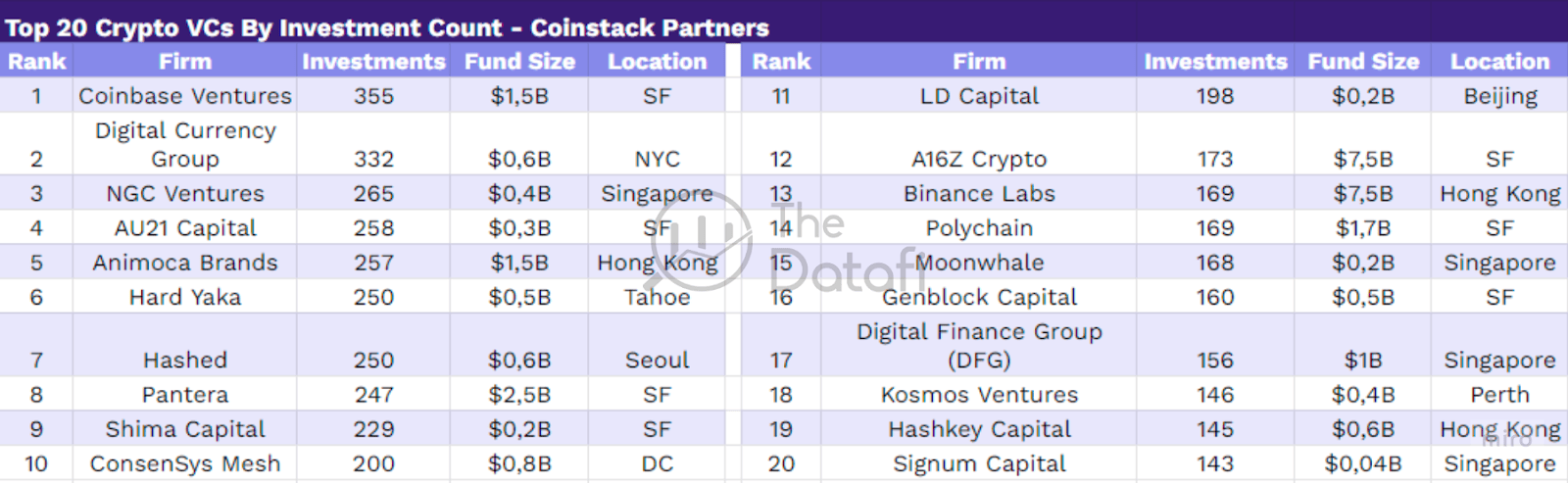

Top 20 VCs with the largest investment fund size

Source: coinstack. Edited by DataFi.

Top 20 VCs with the most investment deals

Source: coinstack. Edited by DataFi.

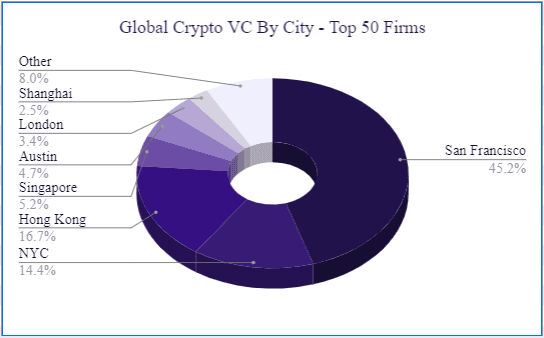

Top 50 cities with significant VC capital for Crypto

Source: coinstack.

Top 20 projects that raised the most funds in Q1 2023

Source: DataFi compilation from Messari, Defillama, and other sources.