Narrative and the Golden Eggs

- Name

- The Datafi

- Published on

- · 19 min read

Author: The Datafi

Published on: April 2023

Summary: Which narratives hold potential and why? At what stage are they? Notable projects within these narratives? Which index/dashboards are used to monitor unusual shifts in a narrative? All will be covered in this DataFi research. Four significant narratives highlighted in this article are RWA, NFT lending, LSD-Fi, L2-L3-Ln.

Introduction

To accompany investors on the finding for "golden eggs," DataFi presents a straightforward yet intriguing study on NARRATIVES - stories that carry trends and money.

Because it's difficult to precisely predict when a narrative will BOOM, DataFi will provide readers with the following information instead:

- Which narratives hold potential which is significant and why do they hold potential? Are they in the early or later stages?

- Notable projects within these narratives and the reasons behind their significance.

- Index/dashboards to monitor unusual shifts which will support your timing.

In this article, DataFi selects four key narratives: L2-L3-Layer-n; NFT-lending; RWA; and LSD-Fi. A summary of reasons for these selections includes:

>> NFT-lending

NFT Lending was ranked in the top 10 of “TVL Market Share Changes of Categories in Defi - Q1 of 2023,” with relatively low TVL. Particularly, true valuable assets are only digitized when approved by the government, requiring robust and reputable operational mechanisms to integrate RWA models later. Could NFT Lending be a transitional step before RWA?

>> RWA

The collapse of Terra (UST) and Celsius highlighted the lending sector's challenges, making Defi in overall have not fulfilled its declaration - “creating an entirely comprehensive financial system”. Based on our research, RWA might hold the primary answer to a more effective future of lending in Defi. Due to its significant responsibility, thoroughly understanding RWA is an essential step.

>> LSD-Fi

LSD-Fi is a narrative previously researched by DataFi in CDOC.14 report. Although there aren't many prominent tokens at the start of 2023, the first "egg" hatched successfully with a 1200% ROI, Pendle. This suggests LSD-Fi might harbor considerable potential despite its current small scale.

>> L2-L3-Ln

Noteworthy events like Arbitrum L3 module, Optimism Superchain, Binance's MVB VI, Rollup-as-a-service projects, Base L2 from Coinbase using Optimism stack, Shapella Upgrade’s block space scheme for L2 proof (blob market) have already shown the potential of their strength and the future phenomenon.

_____________

Research Team: The Research Analyst Team of DataFi, including: Andrew, Tian, and Rosy.

For Further Progress: DataFi hopes to receive feedback from our readers. Contact:

- Admin Rosy (telegram)

- Facebook / Twitter DataFi

- Email: thedatafi@gmail.com

Best regards,

Andrew, Tian and Rosy (from left to right).

I. RWA

1. About RWA

Real World Asset (RWA), a concept dating back to 2019, addressing private credit lending protocols collateralized by real-world assets like Polymath, Maple Finance, Centrifuge, TrueFi, etc. Creating connections of cash flow from real assets to crypto is necessary to expand the applications of digital assets in real life, affirming their value beyond the cryptocurrency market.

The traditional Private credit market size is $1.6 trillion. We should contemplate the potential size of RWA once it officially integrates the cash flows from Private credit to understand its prospect.

Moreover, according to DataFi's study of a Bis.org research, RWA could be a piece of the puzzle to unlock more effective lending, as DeFi still upholds its declaration of creating a comprehensive financial system. This entails a move towards more concentration and regulation, including user identification for asset collateralization and ensuring data accuracy from oracles.

Note: If you are interested in this subject to a significant extent and have an authoritative opinion, please let our team know, and we can review and revise the Bis research article accordingly.

2. RWA Development Phases

Genesis: 2019

This marks the inception of the RWA narrative.

Hot Growth: 2021 - 2022

During this period, impressive growth was observed in various RWA models.

- The peak of active loan value reached $1.4 billion.

- Prominent protocols at that time: Maple on Solana, Truefi on Ethereum.

Loan opening value of protocols in the RWA array for the period December 31, 2020 - March 31, 2023. Source: rwa.xyz

Recession: Post-06/2022 to 12/2022

2022 witnessed the lending platforms (a crucial component of DeFi) becoming the center of chaos, exemplified by the downfall of Terra (05/2022) and Celsius. These events shook market confidence and hindered the development of crypto lending services. This triggered a series of liquidation actions and asset withdrawals, consequently reducing the overall market's and RWA's total loan value (RWA decreased from its peak of $1.4 billion in May 2022 to under $400 million by December 2022).

Notably, within this decline, Maple Finance, which previously held a substantial portion of RWA's loan value, suffered from the collapse of FTX's empire, including Alameda Fund, which significantly impacted lending activities on this platform. Up to now, it has struggled to regain its former momentum.

Next phase: 01/2023 - 03/2023

Overall, the current value of loans in the RWA sector hasn't shown signs of recovery.

Additionally, statistics on the "number of holders" of notable RWA tokens (wCFG, TRU, GFI, MPL) somewhat reflect the opportunities within RWA.

Holder growth over time from 04/2021 - 04/2023. Source: account @j1002 on Dune.

It’s obvious that the number of holders continuously rose from 04/2021 to 04/2023, attaining approximately 24 thousands at present. This is a pretty small figure when compared to a project like Stargate Finance - having more than 25 thousand holders within 1 year.

=> RWA seems to be a new product to crypto investors, meaning that there are still “opportunities” for early investors including us - who are studying on RWA.

3. Notes When Tracking RWA Narrative

3.1. Prominent Projects / Potential

For projects within the RWA narrative, though Centrifuge (wCFG) and Goldfinch (GFI) account for over 80% of the current total loan value market, Maple Finance (MPL) and Truefi (TRU) dominate in terms of new holders since the beginning of 2023.

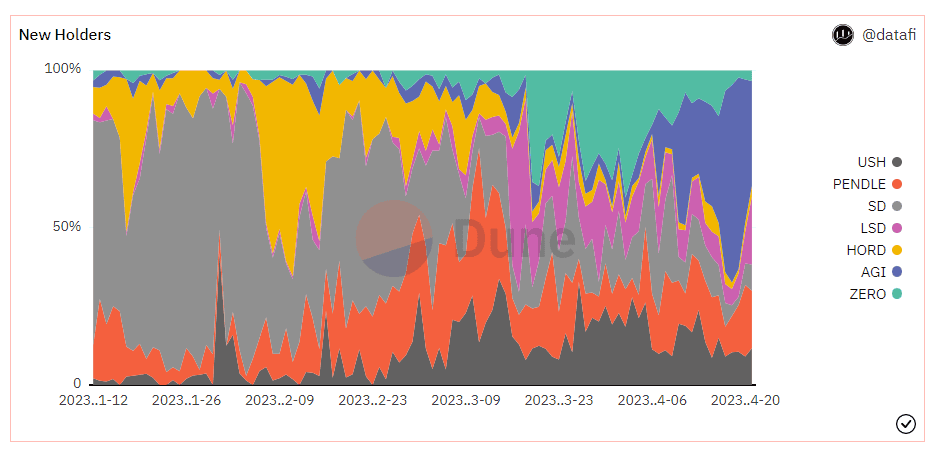

New holders of tokens GFI, TRU, WCFG, MPL period 4/01/2023 - 13/04/2023. Source: Dune, DataFi dashboard.

Furthermore, trading volume statistics for this period also reveal that a significant volume occurs in MPL and TRU.

_

3.2. Key Metrics / Dashboard Links to Follow

You can track RWA through DataFi's dashboards or those of other accounts on platforms like Dune, Flipside, etc. For example: cryptokoryo/rwa.

II. LSD-Fi

Note: Here is the previous report no.CDOC.14 along with new data input.

1. About LSD-Fi

>> Concept of LSD-Fi:

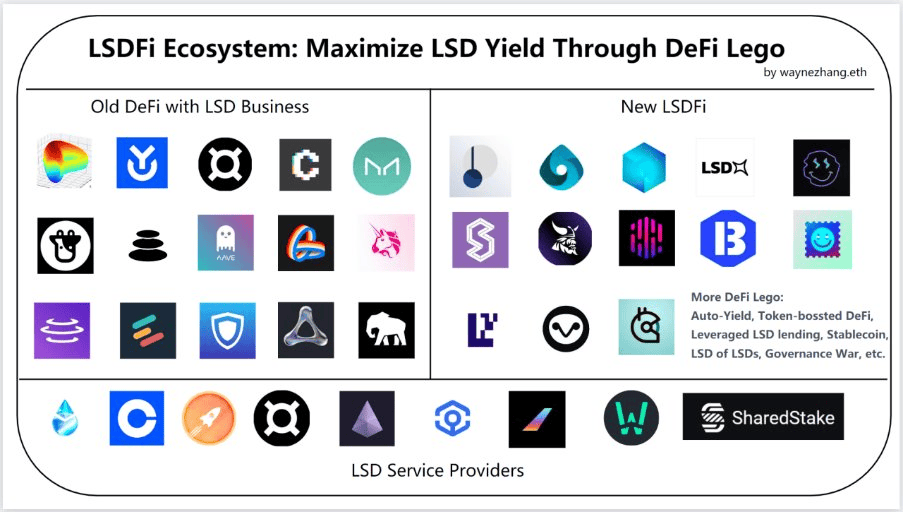

LSD-Fi encompasses DeFi protocols supporting derivative LSD tokens to enhance their integration with other DeFi protocols for optimizing yield (APY). While it's not a new field—tokens like stETH (Lido) and sfxsETH (Frax share) have long been utilized in lending, liquidity providing, and yield strategies, a diverse array of financial products targeting LSDs such as Pendle, Eigen, unshETH, LSDx, etc., have emerged recently.

Ecosystem of LSD-Fi projects. Source: waynezhang.eth

>>Potential of LSD-Fi:

DataFi's assessment indicates that the future market scope for LSD-Fi must be substantial, despite its current relatively small scale, because:

Firstly, other ecosystems have significantly higher staking ratios: Solana has 73.1% SOL staked, Cardano 68.7%, Avalanche 54.64% AVAX staked, whereas Ethereum has only 6.6% of circulating ETH locked within LSD platforms ( 7.9 million ETH, approximately $14.5 billion). This signifies substantial growth potential for LSDs in general and LSD-Fi in particular.

Top 10 Crypto Assets by Staking Marketcap. Source: stakingrewards

Secondly, only a fraction of ETH IOUs is being used within DeFi operations. IOUs are assurance tokens generated through ETH staking; for instance, staking ETH on the Ankr protocol will create ankrETH. While formerly only Curve accepted ankrETH for liquidity, Pendle and many other services with higher APYs have embraced it now. Note: you can refer to the report dated 07/01/2023 (document number CDOC.3) to observe the increasing acceptance of IOUs on more platforms.

In the future, as new services related to these IOUs develop, the decision to "stake ETH in existing platforms for 4%-9% profit" may not require much consideration. New protocols can generate profits ranging from 10-30%, notably Pendle with an APR exceeding 60% for the ankrETH-WETH pair. This could incentivize ETH holders to stake for more substantial gains, reshaping the network to be more decentralized (a goal also pursued by the Ethereum Foundation).

Furthermore, this story is only relevant to the Ethereum ecosystem; other ecosystems transitioning to POS models provide fertile ground for LSD development, particularly LSD-Fi.

2. LSD-Fi Development Phases

Genesis: 2019

Although being introduced early, these solutions garnered limited attention. Perhaps these solutions were noted from the start, but Ethereum hadn't yet executed its POS upgrade, thus lacking a foundational platform for LSD-Fi services to flourish.

Development Phase: 01/2023 - 04/2023

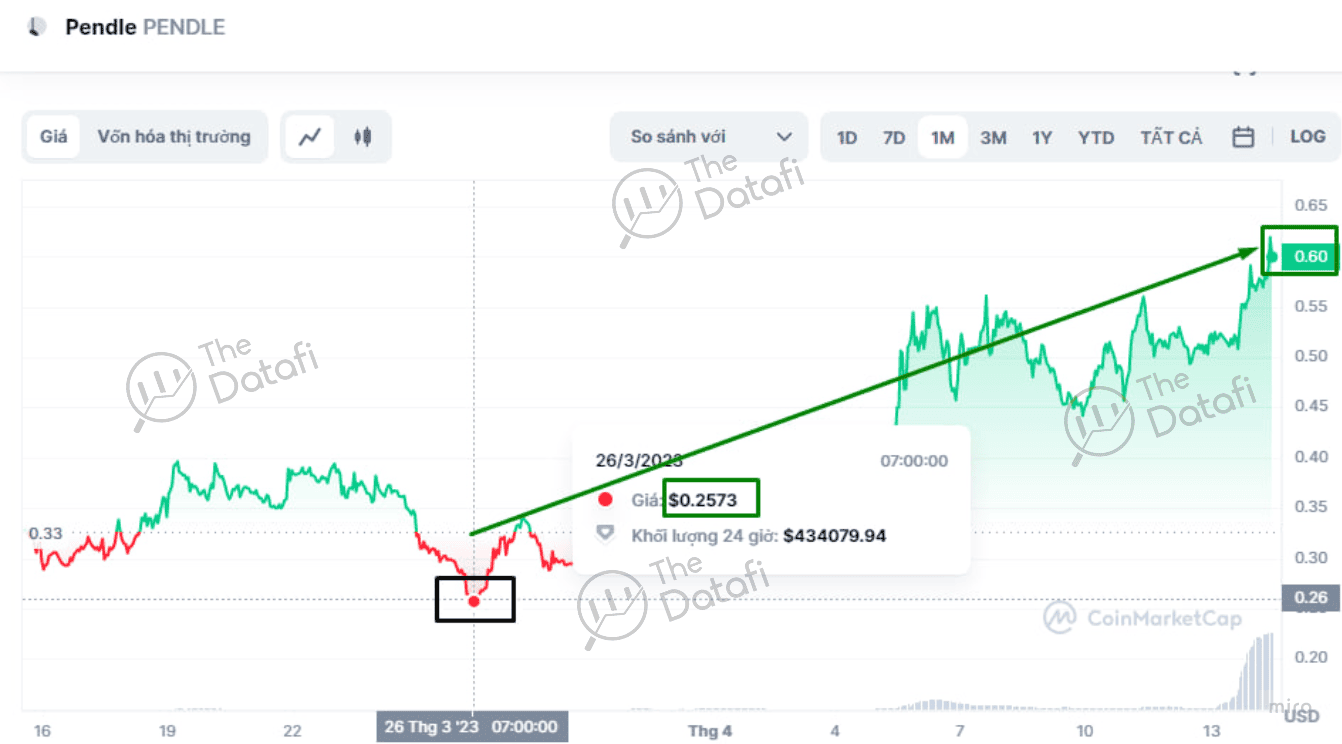

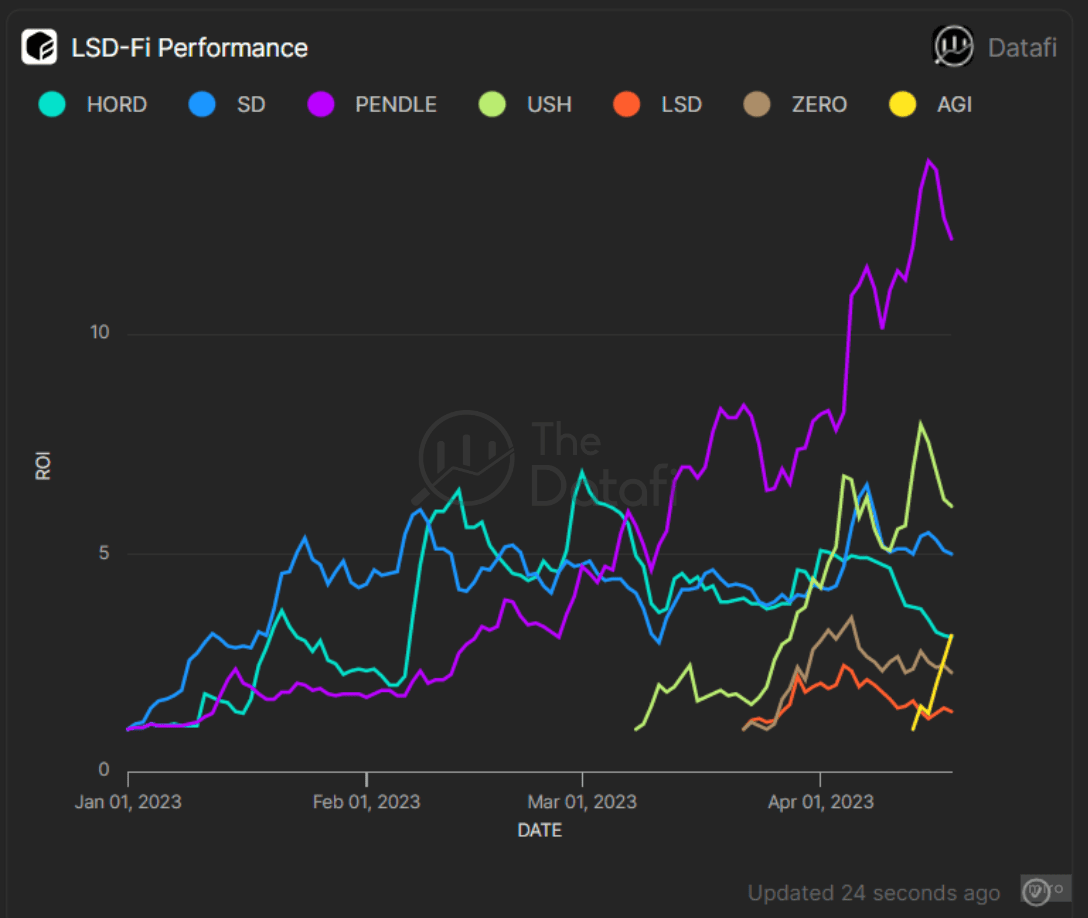

Only during this period do we witness the remarkable growth of various LSD-Fi projects, for instance, Pendle with 1200% ROI - "the first egg has hatched quite impressively".

Additionally, many LSD-Fi projects released tokens in March, such as unshETH (quadrupling in price after three weeks) and LSD (increasing 2.5 times after one week). This reflects definite FOMO in this sector.

_

3. Notes When Tracking LSD-Fi

3.1. Prominent Projects / Potential

Several LSD-Fi projects are attracting considerable trading volume recently on exchanges like USH, AGI, and LSD. Meanwhile, despite substantial growth since the start of the year, PENDLE seems to exhibit a current trend of net selling.

Furthermore, considering the growth of new holders within each project, AGI has experienced a significant surge in new holders over the past two weeks, alongside PENDLE and USH.

Despite PENDLE's considerable selling volume, it has also demonstrated consistent growth in new holders from the beginning of the year until now. This suggests a distribution of PENDLE from whale to retailer is underway in the market.

3.2. Key Metrics / Dashboard Links to Follow

In addition to DataFi's dashboards, you can monitor some other accounts such as: eliasimos/Eth2-Liquid-Staking, unsheth/unshethxyz.

3.3. Which KOL/VC/SM to Follow for LSD-Fi?

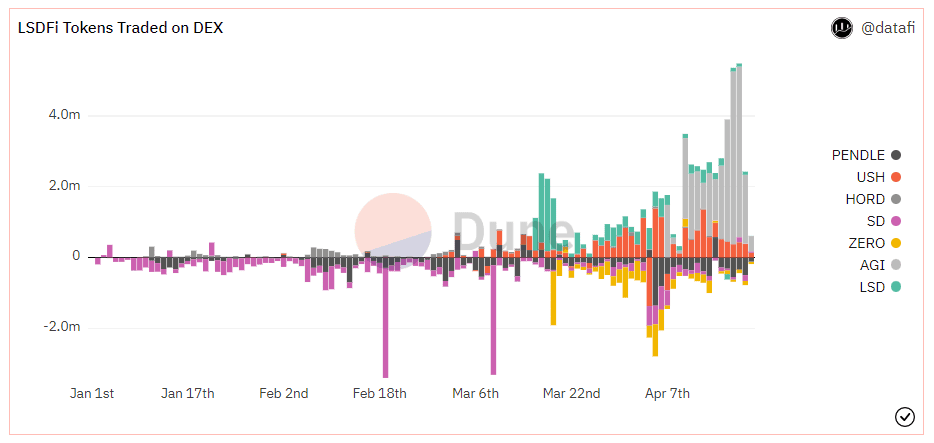

DataFi has examined the activities of smart money on DEXs regarding these tokens, as shown in the figure below:

LSD-Fi trading of smart money on DEXs. Source: Flipside. Dashboard of DataFi

The data indicates that smart money entered LSD-Fi early, but more fervent activity has occurred from early 2023, particularly at the end of March and the beginning of April—coinciding with Ethereum's Shanghai upgradation. Tokens traded during this period include SD, USH, LSD, ZERO, along with the emergence of Pendle, HORD, and the latest addition, AGI. Among these, some wallets you may wish to follow are:

Top Dex Trader USH:

0x30f31d4ce4f72ee8d0ca0040853f3d581008fa3d

III. L1/L2/L3/... Ln - Rollup-as-a-Service (RaaS) or Modular Blockchain

1. L1/L2/L3…/Ln - Rollup-as-a-Service

We all know that the trilemma of blockchain is that it can fulfill 2 out of 3 requirements: decentralization, security and scalability. Many new technologies have been developed to solve this problem, although they are not perfect, such as sharding technology that helps relieve pressure on Ethereum but is not effective when the transaction speed is gradually increasing.

→ Layer2 was born as a solution to this problem.

Layer 2 projects like Optimism, Arbitrum, and zkSync are rapidly developing, reducing the load on the main network. These L2 solutions not only address scalability on L1 but also offer lower fees, faster transaction finality, and better suitability for decentralized applications like DeFi and NFTs in the future.

With the upcoming EIP-1448 (Shapella Upgrade) after the Shanghai Upgrade, alongside the launching of proton-dank sharding, the Ethereum Foundation will allocate a portion of block space (called the blob market) to store proofs on rollups. This indicates the development direction of the Ethereum team, emphasizing that the growth of L2 solutions is essential for Ethereum's expansion and adoption.

Most of the current L2 solutions on the market, such as Optimism, Arbitrum, and ZKsync, are general-purpose rollups. Although there's no specific information about their deployment plans, these L2 rollups seem to be moving towards a rollup-as-a-service (RaaS) business model or allowing Layer 3 (L3) projects to develop over their L2 networks.

Business model comparison between rollup ecosystems on Ethereum. Source: Messari

L3s built on L2 will have superior features such as inheriting security from L1 (Ethereum) and the ability to accommodate the needs of each application (app-specific) such as: reasonable transaction fee and fast finality. Increasing customization for L3s will make Web3.0 applications more accessible to end users, for example, if transaction fees are low enough, application developers can deduct a portion of the profits earned from the application to pay the user, thereby improving the user experience.

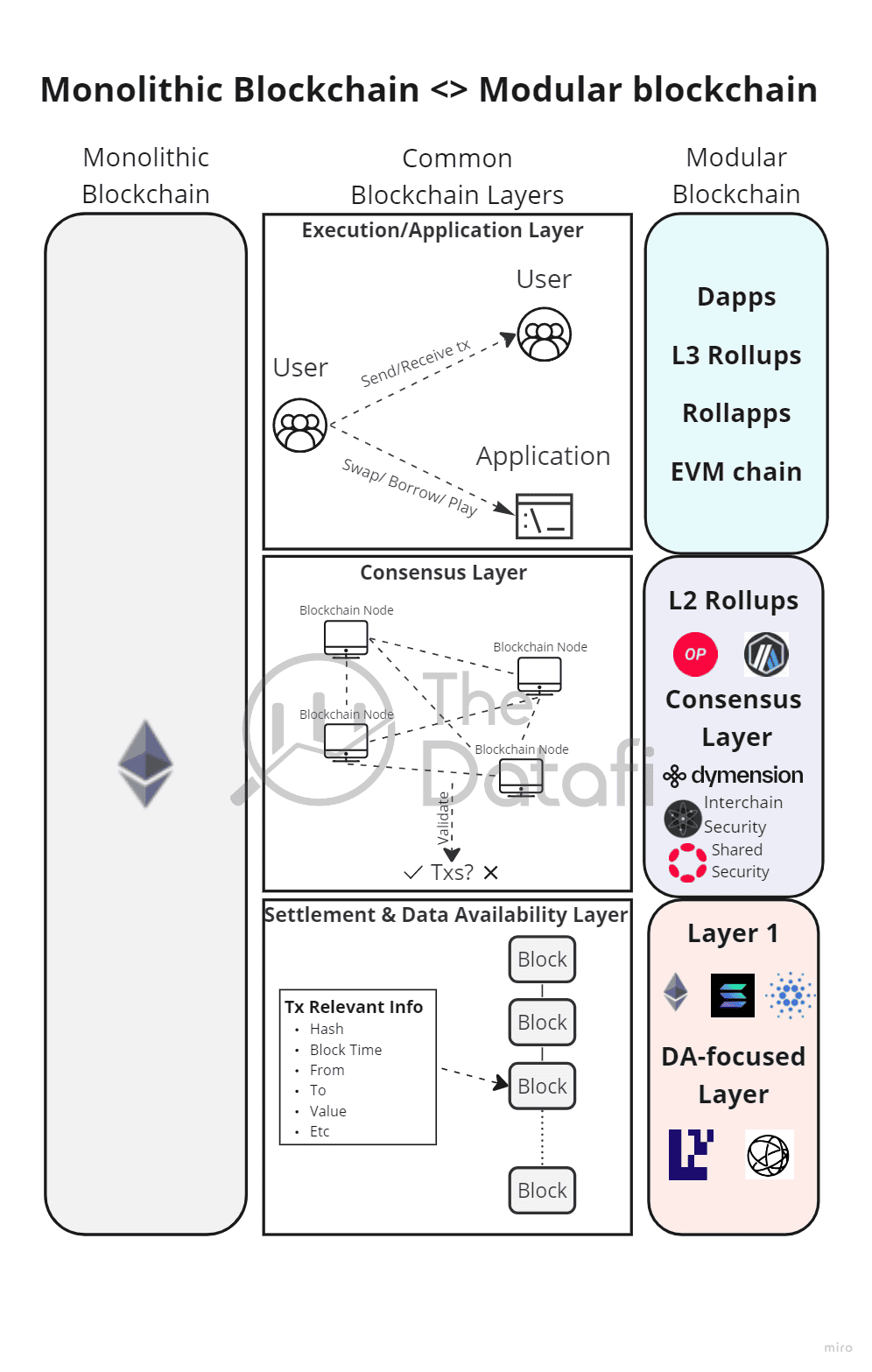

2. Modular Blockchain

As L3 and potentially Ln solutions emerge, it's also a good time for modular blockchain models to develop. Unlike traditional L1 blockchains like Ethereum, Solana, and Cardano, where all tasks like transaction execution, settlement & consensus, and data availability are performed on a single chain, modular models split these tasks into multiple modules executed by specific chains or rollups. This results in higher performance for each module.

The pieces in the modular blockchain model. Source: DataFi

With the potential of post-Shanghai Rollup-as-a-Service models and new infrastructure models like Data Availability, we believe this field will attract investment not only from individual investors but also from organizations.

3. Notes When Tracking This Narrative

3.1. Prominent Projects/Potential

Three NFT lending projects that DataFi recognises potential and EARLY chance for retail investors :

>>ALTLAYER

Regarding the product: Altlayer positions their product as a Rollup-as-a-service with two primary offerings: Flash layer (used for short-term on-chain events like airdrops or NFT minting) and Persistent Rollup (customizable rollup for various applications such as DeFi, GameFi, MetaFi, SocialFi).

Regarding backers: Jump Trading invested $5 million with a valuation of $300 million (Information received from Altlayer team member at Ethereum Conference), Ryan Selkis - Founder of Messari, Sean Neville - Co-Founder of Circle, Gavin Wood - Founder of Polkadot are also backers.

Altlayer is also one of the top 12 finalists in the Most Valuable Builder VI (MVB VI) program recently announced. Typically, projects in the finalist round receive resource support from Binance Labs or direct investments from the funds.

Currently, Altlayer has not yet disclosed a token release plan. However, they have a collection for early users called "Oh Otties!" with an initial minting price of 0.08 ETH. At the moment, the lowest price for 1 Otties is 0.69 ETH (x8.5). Buying an Ottie NFT at this time might serve as a ticket for NFT holders to participate in the public sale if Altlayer introduces a token.

>> CELESTRIA

Regarding the product: Data Availability Layer is built on the Cosmos SDK. Data availability is one of the recent advancements in modular blockchain product development within the past year.

They secured funding: $55 million in series A + B in 2022 from Bain Capital Crypto, Polychain Capital.

Celestria has not yet introduced a token.

>> DYMENSION.

Regarding the product: This is the first Rollup-as-a-service platform on Cosmos. Dymension's product consists of two main components:

- Rollapps RDK: Similar to the Cosmos SDK, RDK allows new projects to build a customized rollapp adjusted to the project's purpose on Dymension.

- Dymension Hub: A chain supporting consensus mechanisms, liquidity, and security features for new rollapps.

Description of Dymension's operational model. Source: Dymension Docs

They secured funding of $6.7 million from Big Brain Holding in February 2023.

Currently, the product is undergoing beta testing, and there is a possibility of introducing a token in May 2023, as indicated by some posts on the project team's Twitter.

IV. NFT LENDING

1. About NFT Lending

With the explosion of the NFT market over the past few years, NFT lending is no longer an unfamiliar term. In terms of operation, NFT lending protocols share many similarities with DeFi lending, users collateralize assets - in this case, NFTs - and borrow other assets such as stablecoins, ETH, etc. for short-term transactions for expenditure or leverage.

In terms of operational models, NFT lending protocols can be divided into three main types:

Peer-to-Peer Lending (NFTFi, etc.)

This is a direct lending arrangement between individuals. The NFT owner (borrower) establishes a loan contract, including terms such as loan duration, interest rates, etc., through a smart contract. When the lender agrees to the terms, the borrower's NFT is transferred into the smart contract until the borrower repays the loan according to the contract conditions.

Advantages:

- Independent of oracles.

- Can be extended to most types of NFTs, not just blue-chip NFTs.

- Protocols are not exposed to bad debt risks.

- This is the easiest-to-implement and manage model among the mentioned ones.

Peer-to-Pool Lending (BendDao, etc.)

Similar to Aave v2 or Compound in DeFi, NFT lending protocols in this category share a liquidity pool. Here, borrowers collateralize NFT assets and borrow other supported assets from the pool at an interest rate determined by the protocol.

>>Advantages: This model is more flexible than peer-to-peer since borrowers don’t need to find appropriate lenders. Instead, the protocol proposes terms and contracts to the borrower.

>>Disadvantages:

- Protocols can face issues with bad debt concerning low liquidity assets on-chain.

- Protocol liquidity is not self-driven and depends on third-party liquidity providers.

Peer-to-Protocol Lending (JPEG’d)

In this model, quite similar to MakerDAO's operation, the protocol allows lenders to collateralize NFTs and borrow stablecoins from the protocol.

>>Advantages: Protocol liquidity is more proactive as it doesn't depend on initial liquidity providers.

>>Disadvantages: The protocol needs to enhance stablecoin liquidity and build an ecosystem around its stablecoin.

2. Development Stage of NFT Lending

The number of users participating in NFT lending is increasing, reaching its peak in the first quarter. 2023.

Number of borrowers and lenders per month from 05/2020 to 04/2023. Source: @rchen8

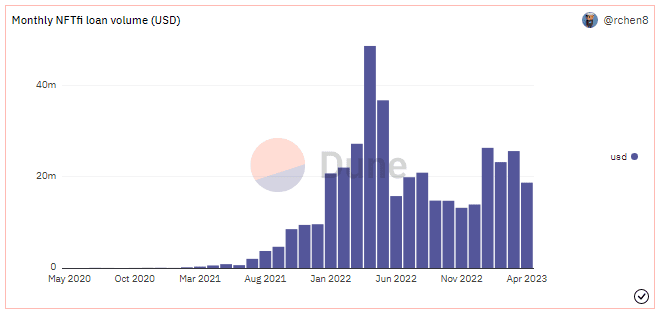

Although the NFT-fi lending volume hasn't surged as it did in 2022, it has recovered. Additionally, the increasing user participation in NFT-fi indicates growing acceptance and application.

Monthly NFT-fi lending volume from 05/2020 to 04/2023. Source: @rchen8

3. Notes for Monitoring This Narrative

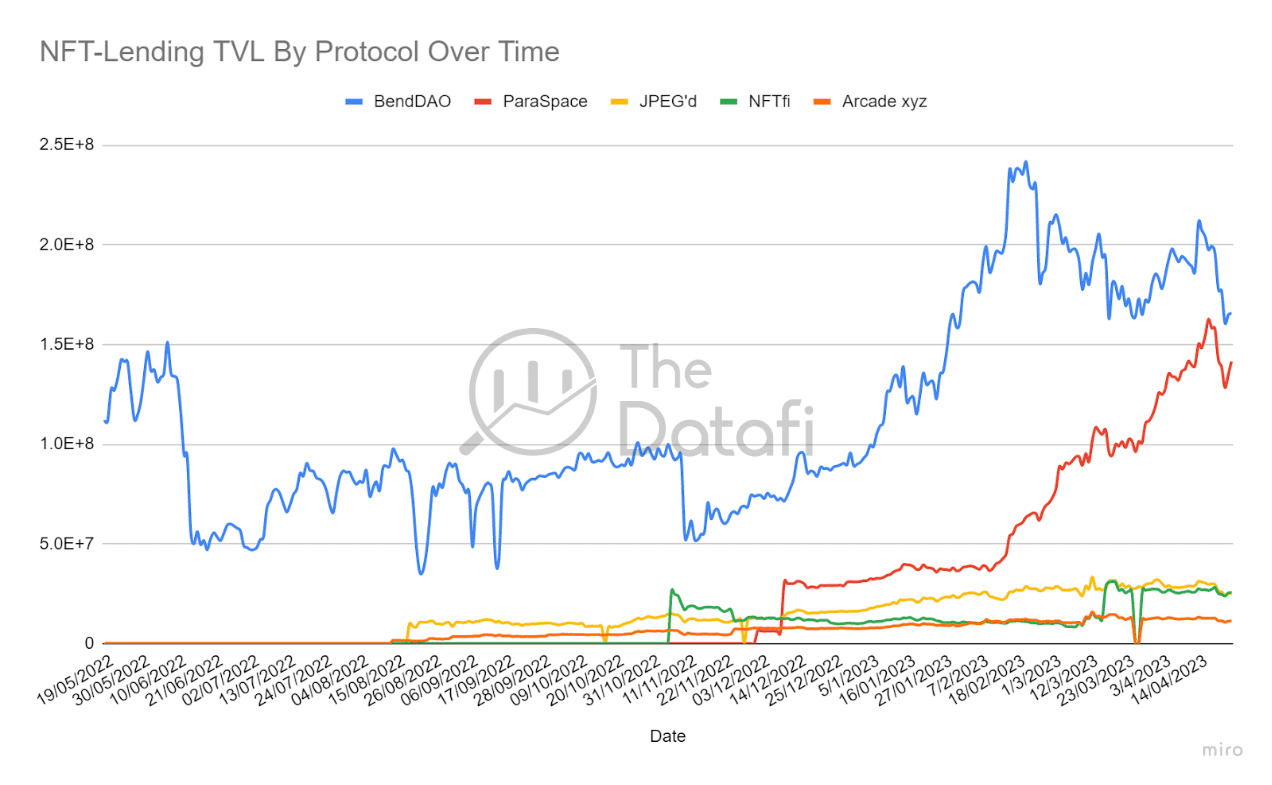

In this research, DataFi will examine the top 5 NFT lending protocols with the largest Total Value Locked (TVL) in the current market (according to Defilamma statistics): BendDao, JPEG’d, Arcade Finance, NFTfi, and Paraspace.

From historical data, most of these protocols have emerged from April 2022 to the present, with BendDao being the earliest. So, how is their development progressing?

>> Assessing TVL

BendDao has maintained its position as the protocol with the largest TVL in the market since its project deployment. Alongside, ParaSpace is also notable, with TVL rapidly approaching that of BendDao in just ~3 months since deployment.

Furthermore, NFTfi has shown substantial TVL growth since early April. Notably, both these protocols have not yet introduced tokens.

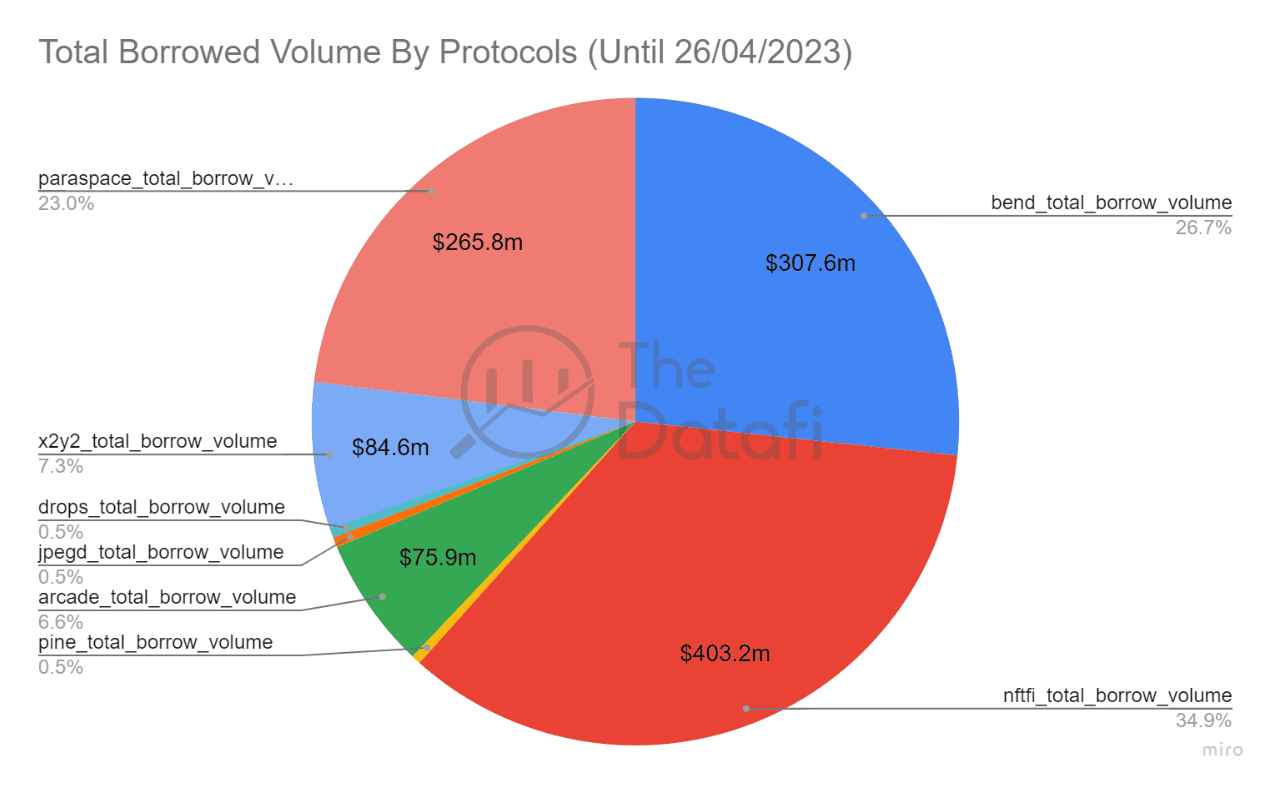

>> Assessing Borrowing Volume

As of now, within this sector: NFTfi leads with a borrowing volume of over $400 million - accounting for 35% of the total borrowing volume, followed by BendDao (27%), ParaSpace (23%), and X2Y2 (7.3%).

>> Assessing Borrowers

DataFi chooses to assess borrower growth over lender growth because: :

In NFT lending protocols, user participants include both lenders and borrowers. Lender growth is related to liquidity and protocol maintenance costs, while borrowers typically represent the protocol's "cash flow" (fees earned from borrowing activities). Thus, increase in borrowers reflects the protocol's revenue growth at present and potentially in the future.

Comparing borrower growth between NFT lending models shows that:

The peer-to-protocol lending group (BendDao and ParaSpace) has the highest potential for growth in new borrowers compared to other models.

In general, among NFT lending protocols, only three protocols currently have over 1K unique borrowers: BendDao, Paraspace, and NFTfi. Paraspace, particularly, has recently exhibited rapid and continuous rise, over a span of just approximately 3 months from late December 2022 to April 2023. In contrast, other protocols like BendDao and NFTfi took from 6 months to 1 year to attract substantial borrowers.

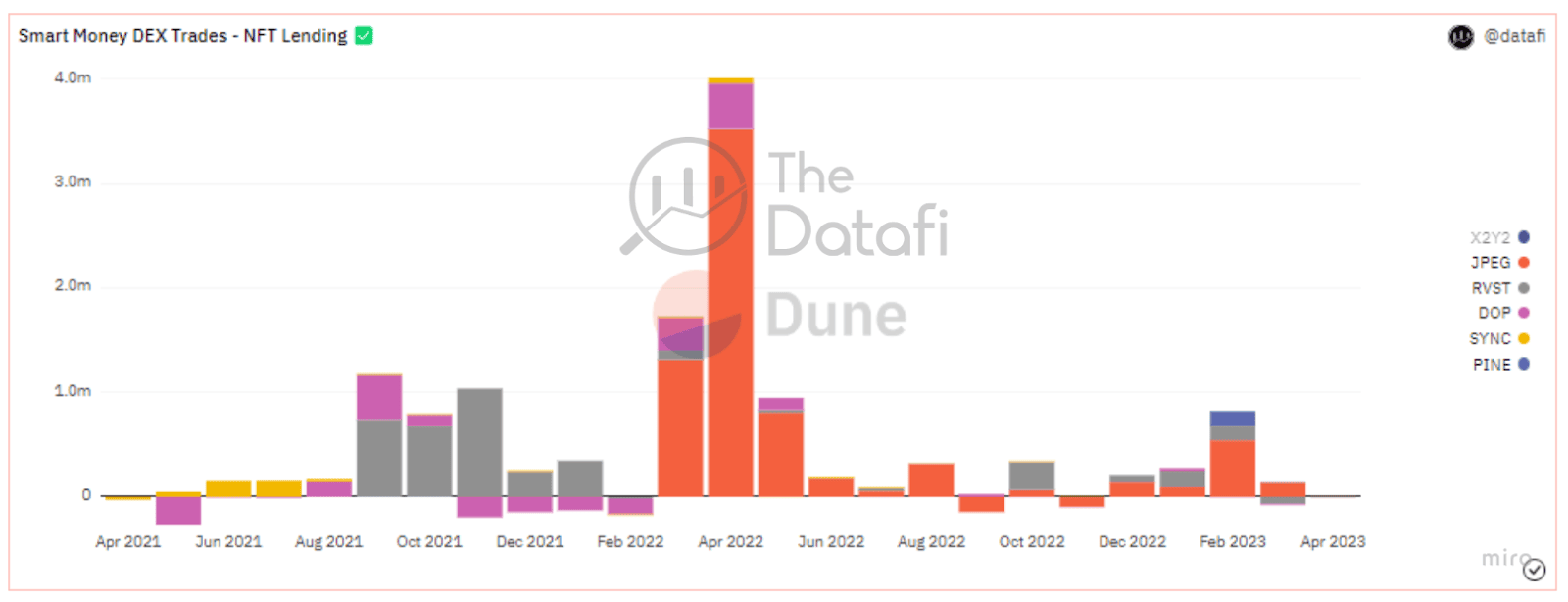

>> Top Tokens with Smart Money Trading

Eventually, how has smart money engaged in the NFT-lending field?

A total of 7 out of 20 NFT Lending protocols have tokens, including: JPEG, X2Y2, FRAKT (FRKT), Drops (DOP), Revest Finance (RVST), Pine Protocol (PINE), SYNC Network (SYNC). DataFi has aggregated information and found that smart money has mainly engaged with X2Y2 and JPEG tokens. They conducted most of their trading in 2022.

Note that while X2Y2 saw early accumulation of smart money, its selling volume is currently quite low.

Furthermore, when excluding X2Y2, focusing on the remaining tokens reveals that RVST was accumulated as early as 2021 and hasn't seen significant volume return. Similarly, JPEG was primarily accumulated in 2022, with renewed accumulation starting in February 2023 with insignificant selling volume.

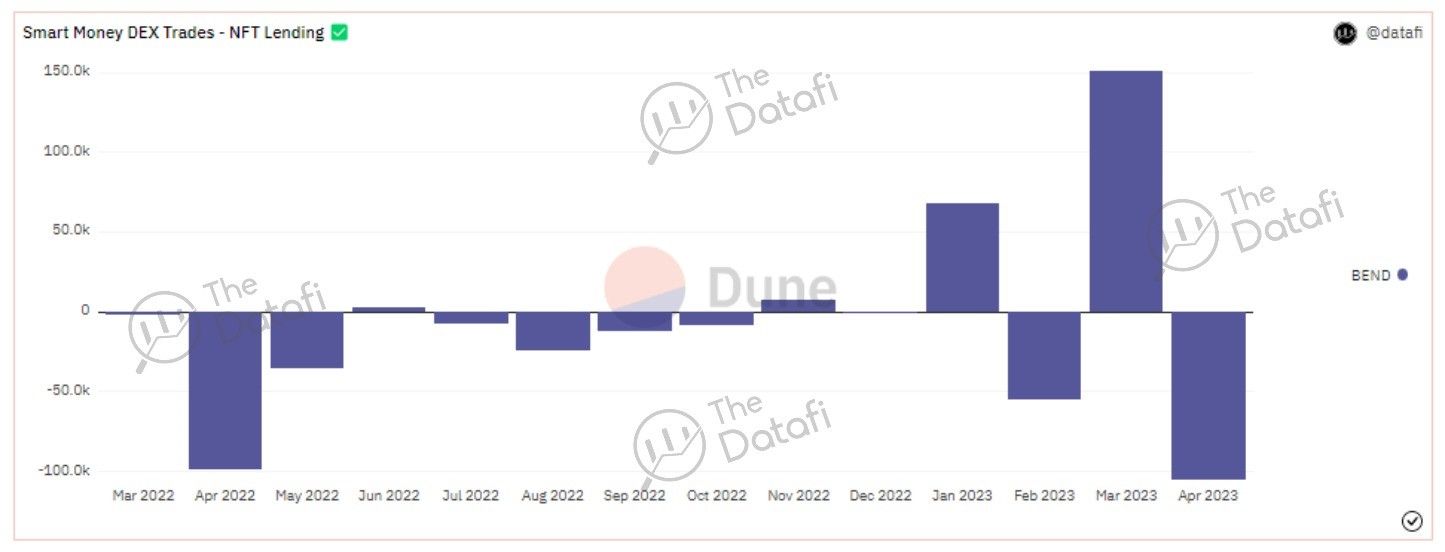

Update: BEND trading activity of smart money.

Source: Dune. Dashboard of DataFi

Overall, it seems that smart money is awaiting the NFT lending season, holding their positions primarily.

Finally, we wish you a new journey filled with lessons and achievements! Don't forget to seek more insights and opportunities in other research conducted by the team, such as Big Signal 2 (macro), Money Flow, and Venture Capital, which were recently published in April 2023.

Thank you, dear readers!

Disclaimer: This article is not intended as financial investment advice.